The Philippines is the 13th largest country in the world, with a population of over 100 million people — yet just 2% have access to credit cards. Like most emerging markets, the country still operates primarily as a cash-based economy. As a result, even those on the high end of the pay scale, with proven track records of repaying debts and stable incomes, must show significant assets or are denied access to credit. This system reveals a clear catch-22: you can’t build a credit history without a credit card, and you can’t get a credit card without a credit history.

Financial services firms in these markets also face their own operating issues given this limited consumer credit history, as well as the challenges that come with integrating current technology — i.e., digital wallets. These systemic challenges manifest as a massive barrier to upward mobility for average consumers: without any method to prove creditworthiness, they are impeded from access to capital that can be used for essential investments in their daily lives, like a home or car.

Enter TMV’s latest investment Plentina, co-founded by Kevin Gabayan and Earl Valencia, who set out to enable growth in emerging markets by leveraging the power of data. Leaning into their collective expertise in machine learning — Kevin worked in data science at Bump Technologies and Google, Earl led digital transformation at Charles Schwab — the two developed a platform that allows consumers to access and repay BNPL (buy now, pay later) installment loans through electronic wallets and voucher codes. This structure offers the financial advantages of a credit card, helps to avoid predatory lenders and, unlike other models, has no hidden fees, allows easy repayment and helps consumers build credit history.

From Palo Alto to Manila

Kevin and Earl first met while pursuing post-graduate degrees at Stanford, and quickly learned they shared the same drive to enable better outcomes for consumers in emerging markets. As they delved further into the tech world, they noticed the marked absence of Filipino representation, and sensed an urgency to take action to help move the country’s infrastructure forward.

Kevin, quoting Kiva’s Jessica Jackley, remarked: “There is always something you can do. As long as you’ve identified an injustice and are willing to educate yourself to solve it, there is an opportunity to make it happen.” Driven by a desire to use his professional experience to create impact, Kevin left Google and went back to the Philippines. There, he spent time talking with hundreds of people on the streets of Manila, learning about the daily needs, hopes and challenges of average consumers, and found that many were either in a futile competition with those who already had a financial advantage or had fallen into predatory debt traps. In parallel, he and Earl — who had also spent time in the Philippines before returning to the US — were witnessing the reinvention in the western world of BNPL models like Afterpay, Klarna, Affirm and others. In conversations, the two realized that what was preventing these models from translating to emerging markets was a lack of data: versus a country like the U.S., where 90% of the population is listed in a credit bureau, in the Philippines, that number is just 13.5%.

How it Works

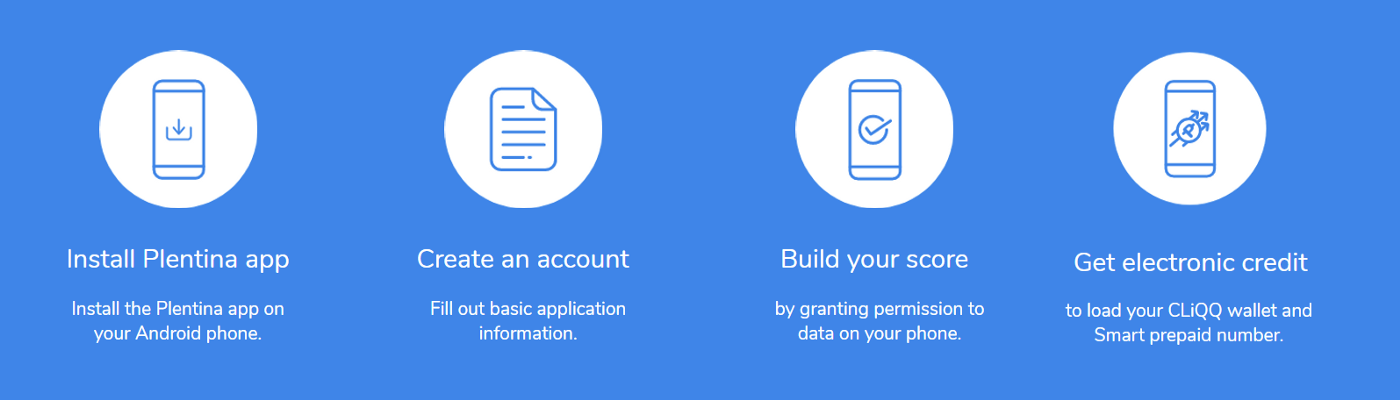

The data had to come from somewhere else. Kevin and Earl developed an Android app that works with legacy systems to support the BNPL model in markets where few have credit scores and/or merchants can’t easily integrate technology. Leveraging consumer data from alternate sources, like retail loyalty programs, mobile data (with user permission) and other partnerships, Plentina has generated over 10 million credit scores to date. On the backend, the platform uses machine learning models to gauge the creditworthiness of loan applicants, using these alternate data sources in lieu of credit histories.

To the Philippines, and Beyond

Plentina launched in the Philippines in October of 2020, initially focusing on small daily purchases at partner vendors, including 7-Eleven. Since then, they’ve added over 20 brands and additional categories — beyond groceries and educational supplies — to include travel and e-commerce, among others. In 2021, Plentina’s app downloads increased by 500%, from 30k at the end of 2020 to over 150k users today. Recognizing that access to credit in emerging markets presents a global problem that stretches far beyond the Philippines, Kevin and Earl plan to continue expansion of Plentina throughout Southeast Asia and beyond. As Plentina grows, they will offer additional financial services for the economies they serve. And, their approach is already getting noticed stateside; Plentina was twice featured in TechCrunch as well as in Times Square via Nasdaq.

We asked Kevin and Earl what advice they’d give to new founders. Here’s what they had to say: “You have to be aligned on your vision and how you envision it actually coming to life,” they agreed. “The right team is everything.”

Written by Soraya Darabi, General Partner and Founder of TMV